Welcome to this post on the danger of mutual fund fees. One important aspect of learning how to invest, and one that is often overlooked, is the role that high fees play in derailing a person’s financial plan. There are costs associated with owning investments. Anytime a person buys or sells stocks they pay commission fees. If you own mutual funds, there are management fees and various commissions associated with those investment products.

When you buy property, you pay fees to acquire it and sell it. If it is a rental property you may also pay fees to have someone else manage it. Fees are a fact of life when it comes to investing and our jobs as investors are to get the most bang for our buck by minimizing, to the greatest extent possible, the amount of money that we pay in fees. An easy way to do this is to own low-cost mutual funds or exchange-traded funds (ETFs).

Why You Should Care About A Percentage Point!

The entire investment industry exists to line their pockets with your hard-earned money which brings me to my first point. The problem with investment fees is that they are not transparent. In fact, they are usually buried in financial paperwork that takes a room full of lawyers and accountants to figure out. This only serves to disguise their corrosive impact on your investment returns.

The second danger about investment fees is that, at first glance, they seem relatively benign. Mutual fund fees range between 1.5% to 3% and average 2%. A co-worker once told me that there was no point in ditching his mutual funds over a measly percentage point and therein lies the problem with investment fees. They seem relatively harmless – as being so small that they aren’t worth the effort to move funds or to take control of your own investments from your advisor.

In reality though, investment fees are a silent killer of long term investment returns. I equate high fees as a type of risk to an investment plan because their effects are similar to that of inflation or worse. Just as inflation slowly erodes our purchasing power over time, investments fees cripple our compound returns over time. Former Vanguard CEO John Bogle offered one of the greatest insights ever when he said that “the miracle of compounding returns is overwhelmed by the tyranny of compounding costs.”

That’s why the type of investments you select should always be the low-cost option. I say this for 2 major reasons. First, as mentioned above, mutual fund fees are a real killer when it comes to investment returns over time. Second, it’s a proven fact that very few active mutual fund managers can actually beat the index on a consistent basis, net of fees. So why pay up to 2.5-3% in fees for performance that you could reasonably expect to get for a fraction of the cost.

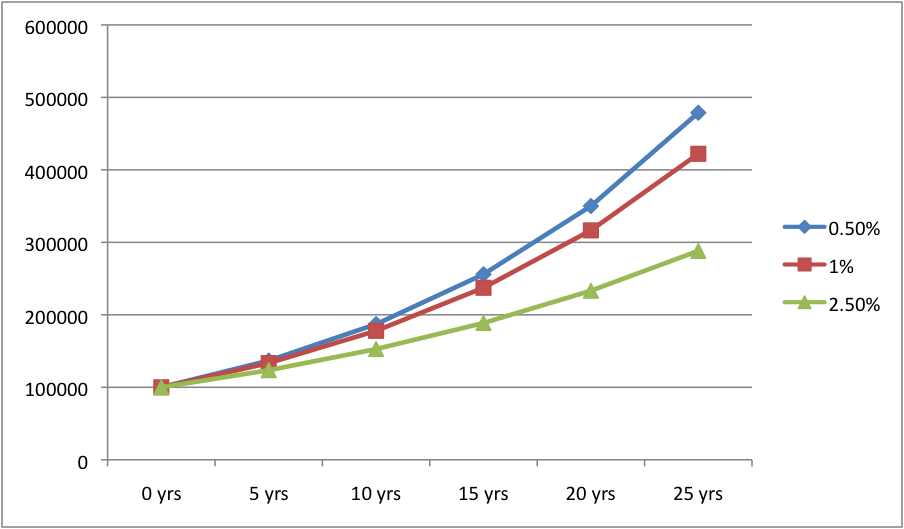

Between inflation and high fees, the odds can really stack up against an investor, so always make sure you have low-cost index funds or ETFs. Low cost means management fees that are under 1% and, in most cases, you’ll find index funds or ETFs for under 0.50%. The chart below runs 3 scenarios that illustrate the impact of mutual fund fees on investment returns over a twenty-five year time frame. The calculations assume a 7% annualized rate of return.

Click to Enlarge

As can be seen, the most significant impact on investment returns is between the 0.50% MER and 2.5% MER. It’s the difference of nearly $200,000! Basically for every half a percentage point that you pay in fees, you’ll end up with $50k less over 25 years. This example goes to show that, what may seem like an insignificant fee can make a major difference on your investment returns over time. If you’re interested in running your own scenarios, check out this awesome mutual fund fee calculator at Bankrate.com.

Mutual funds really suck and I am a strong believer of low cost ETFs. Great ETFs such as VTI and VCE, VCN can even generate higher return than portfolio that consists of solid dividend paying companies. That 200K difference is really big that I feel so bad for people who invest in mutual funds. They will have to be informed and make a sound decision for their future. Thanks for the great read!

BeSmartRich

Thanks for the comment. My first foray into investing happened in the late 1990s and I can’t believe that I was paying 2.5%-3% for an INDEX FUND! I’m glad I learned about low-cost investing options, they will save me thousands of dollars over time.

From my experience some mutual funds are pricey relative to index funds, but one caveat many people rule out is that those expensive mutual funds pay more in capital gains and dividends. I feel as long as you have funds with expenses under .90%, that has good growth, and pays good dividends it can still be worth it. Just don’t invest it all into 1 fund, mix it up within the portfolio with cheaper vanguard and fidelity funds that are .25% or less to give you a good balance. I’ve witness two separate funds with the same amount invested, whereas the index fund gives you 800 dollars in dividends a year, but the mutual fund gave you 1200 in dividends a year. In this case your paying more but your earning more as well.

You make an interesting point here. You could get more in dividends by owning a certain type of mutual fund that focuses on dividends. But you may not get the same growth rate as you would if you owned the index. It’s a proven fact that fund managers can’t beat the index consistently over time and once you add in the additional fee for trying I just don’t see the value there. I think you could be sacrificing capital gains for dividends here…Anyone else want to weigh in on this?